Afton has partnered with the Illinois State Board of Education since Summer 2017 in developing and implementing its plan to meet the site-based expenditure reporting requirement of ESSA. Currently in Illinois, as in most states, public education finances are reported at the local education agency (LEA) / school district level. With the implementation of ESSA, school-level expense reporting will be required. ISBE has created an intentional process to make sure the state and its districts not only meet the requirement but find value in it as well.

Arguably, the most critical component of ISBE’s approach has been the creation of a value proposition for site-based expenditure reporting. An advisory group comprised of key stakeholders has been guiding this work from the onset, and co-created the following shared value proposition:

- Site-level expenditure reporting provides an excellent opportunity for LEAs to maximize care for the whole child, in a whole and healthy school, nested within a whole and healthy community.

- With site-level expenditure reporting, how resources are allocated will be more readily accessible and revealing to schools and stakeholders.

- This reporting should ultimately lead to greater equity and improved outcomes for kids: it empowers LEAs and communities to assess and improve equity in funding between individual schools, and it enables a better understanding of the relationship between student outcomes and financial resources.

- It will also enable LEAs, schools, and the state to identify evidence-based best practices and opportunities to foster innovation between peers.

ISBE is intentionally encouraging local responsibility and dialogue about resource allocation. Notably, because the advisory group identified the value as primarily for LEAs and communities (and explicitly not for the state agency), decisions forming the plan for site-based expenditure reporting have been made through these lenses.

As we get closer to the reporting timeframe in Fall 2019, ISBE and the advisory group have shifted our focus from developing Guidance (or “rules”) for reporting development to helping prepare districts for both completing the reporting and making meaning of it – thereby making strides in realizing the value proposition. Two key mechanisms are enabling this focus, and both are guided by the value proposition: data visualization and training.

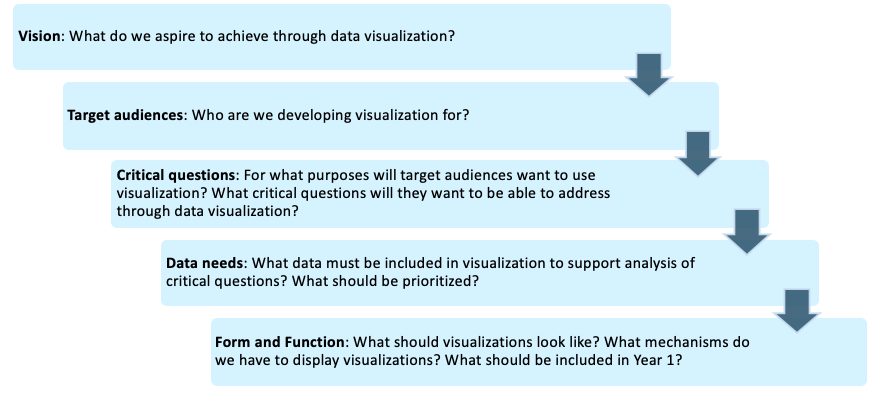

Data visualization is “where the rubber meets the road” for this initiative – where our value proposition comes to life and the data become public, contextualized, and actionable. Our process to create visualizations was intentional, aiming to answer the following questions:

- What are the conversations that are aligned with the value proposition that we want to encourage?

- What data are necessary to contextualize and inform these conversations?

- Among these data possibilities, what should be prioritized for Year 1 Reporting?

ISBE and the advisory group worked through a framework containing a series of exercises to answer these questions. This framework is shown below.

Following this framework allowed ISBE to design draft visualizations grounded in a shared understanding of priorities.

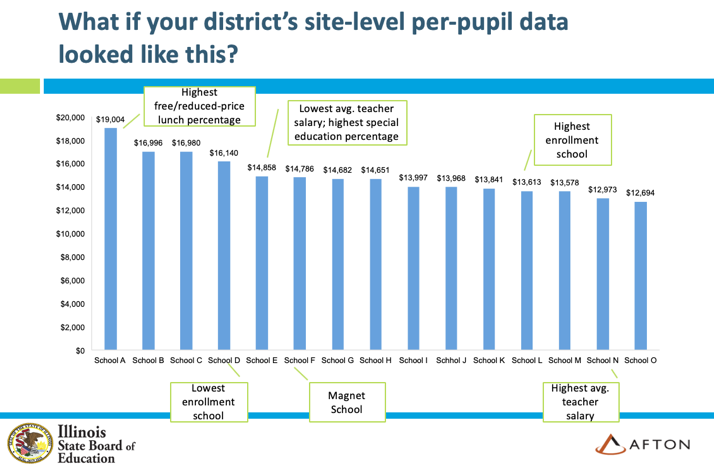

Training is the other critical component enabling LEAs and other local stakeholders to make meaning of site-based expenditure data. ISBE believes district leaders are best positioned to lead their local communities in dialogue about data outcomes and making meaning of the data. While the focus of training can easily default to technical capacity building, our ISBE/Afton team believes that equipping district leaders with the tools necessary to understand what this data is telling them, in order to make informed decisions about future resource planning, is pivotal to the success of this initiative. Consider, for example, the following real data set from an Illinois district (anonymized).

Before this data becomes public through site-based expenditure reporting, ISBE is helping districts prepare to acknowledge the types of questions the data will beg – from themselves, and from other stakeholders. Through thoughtful analysis of site-based expenditure data alongside contextual data on student needs and academic outcomes, the goal is for local leaders to be able to determine if outcomes of resourcing decisions (seen through site-based expenditure data) promote equity and are aligned with their intended strategic priorities. If not, LEAs should be equipped to determine if resourcing decisions should be reevaluated or if strategic priorities should be reevaluated in light of actual data on equity and outcomes. By doing so, we will see meaningful progress toward the value proposition.

For districts considering how to make this new reporting requirement meaningful, regardless of your state’s approach to developing the reporting, Afton recommends the following:

- Develop a local value proposition for this data – what does your district and community want to do with the data? For example, evaluate equity, evaluate the relationship between spending and outcomes, or something else?

- Facilitate early exploration of your site-based expenditures.

- What, approximately, has your district been spending by site?

- Considering contextual data such as student needs and academic outcomes, what can you hypothesize about equity? About the relationship between spending and student outcomes? How can you explore these hypotheses?

- Are there any intentional changes you may want to make during this year or in anticipation of budgeting for next year?

- Suggest Cabinet-level discussions of what the early exploration reveals. Don’t be caught off-guard when data becomes public.

- Acknowledge that data, when available, will need to be unpacked and evaluated, and be transparent in the process of doing this.

- It may be helpful to form an advisory group of stakeholders to guide this process to ensure community involvement in understanding and making decisions based on the outcomes of this work. At minimum, ensure transparency into the analysis process.